|

|||

|

|

|

||

|---|---|---|

|

||

|

||

|

||

|

||

|

||

|

|

|

|

Refinance Home to Pay Off Debt: A Comprehensive GuideRefinancing your home to pay off debt can be a strategic move to improve your financial health. This guide will explore the benefits, considerations, and processes involved in refinancing your home loan. Understanding Home RefinancingRefinancing involves replacing your current mortgage with a new one, often with better terms. This can free up cash to pay off high-interest debts such as credit cards. Benefits of Refinancing

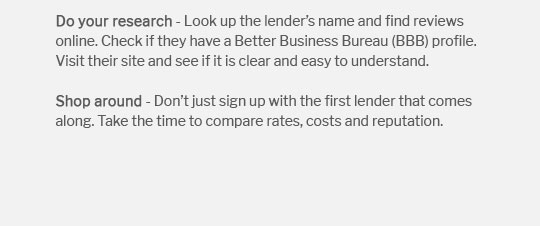

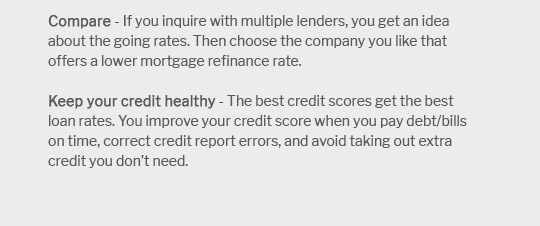

Considerations Before Refinancing

Steps to Refinance Your HomeTo successfully refinance, follow these steps: Evaluate Your Financial SituationUnderstand your current debts and how refinancing will impact them. Assess whether a va refinance mortgage loan could be beneficial. Shop for LendersCompare rates and terms from different lenders to find the best deal for your situation. Apply for RefinancingSubmit your application, providing necessary documentation such as income statements and tax returns. FAQCan I refinance with bad credit?Yes, but options may be limited. Consider improving your credit before refinancing to secure better terms. How does refinancing affect my mortgage term?Refinancing can either shorten or extend your mortgage term, depending on the new loan conditions. Is the VA streamline mortgage refinance program an option?Yes, if you qualify, the va streamline mortgage refinance program offers simplified refinancing for VA loans. ConclusionRefinancing your home to pay off debt can be a wise financial decision, but it's important to weigh the pros and cons. Evaluate your financial situation, explore all options, and consult with financial advisors if necessary to make the best choice for your needs. https://www.equifax.com/personal/education/credit-cards/articles/-/learn/mortgage-refinance-consolidate-credit-card-debt/

Highlights: - Refinancing is the process of taking out a new mortgage and using the money to pay off your original loan. - A cash-out refinance where you take ... https://www.rocketmortgage.com/learn/refinance-to-pay-off-debt

You can refinance to consolidate debt, taking on a larger mortgage in return for a potentially more manageable way to handle debt. https://www.apmortgage.com/blog/should-i-refinance-my-home-to-pay-off-high-interest-debt

Using home equity to pay off high interest credit card debt can be a great move for homeowners who can swing their new monthly payments and plan to stay in ...

|

|---|